Understanding Early Repayment Charges on Mortgages: A Comprehensive Guide

Last updated: July 2026

Reviewed by: [Dr. Gideon C., Ph.D., MSc, MBA, FCCA, CAMS]

An early repayment charge (ERC) is a fee your mortgage lender may charge if you repay your mortgage, remortgage, or overpay beyond the permitted allowance before your mortgage deal ends. ERCs are commonly between 1% and 5% of the outstanding balance, depending on your lender and mortgage product..

Quick answer: What is an early repayment charge?

An early repayment charge is a fee charged by mortgage lenders when borrowers repay their mortgage early, leave a fixed-rate deal, or exceed permitted over payments. ERCs are normally calculated as a percentage of the remaining mortgage balance.

In this article, we will delve deep into the intricacies of early repayment charges on mortgages, explaining what they are, how they work, and the potential penalties for paying off your mortgage early. We will also explore ways to avoid these charges and provide tips for minimizing their impact.

Early Repayment Charge Calculator

Early Repayment Charge (ERC) Calculator

Calculate actual penalty exposures when overpaying or exiting a property deal early. Accounts for standard UK penalty-free overpayment allowances.

Your Financial Computation

Table of Contents

- What Are Early Repayment Charges (ERCs)?

- How Do Early Repayment Charges Work?

- Why Do Lenders Impose Early Repayment Charges?

- Types of Mortgages with Early Repayment Charges

- How Are Early Repayment Charges Calculated?

- Pros and Cons of Early Mortgage Repayment

- How to Avoid Early Repayment Charges

- What to Do If You’re Hit with an ERC

- ERCs and Remortgaging

- Is Paying Off Your Mortgage Early Worth the ERC?

- Case Studies: Examples of ERCs in Practice

- Frequently Asked Questions about Early Repayment Charges

- External Resources for Further Reading

- Conclusion

1. What Are Early Repayment Charges (ERCs)?

Early Repayment Charges (ERCs) are fees charged by lenders when you repay your mortgage early, either by paying off the loan in full or by making overpayments that exceed the allowed limit during a specific period. These charges are common in fixed-rate mortgages but can also apply to variable-rate mortgages, tracker mortgages, and other types of loans.

2. How Do Early Repayment Charges Work?

ERCs are typically a percentage of the outstanding loan amount, and the rate often decreases the longer you have held the mortgage. For instance, an ERC might be 5% of the remaining loan balance in the first year, decreasing by 1% each subsequent year until it reaches zero. However, the exact terms vary depending on the lender and the specific mortgage product.

3. Why Do Lenders Impose Early Repayment Charges?

Lenders impose early repayment charges to protect their financial interests. When you take out a mortgage, the lender expects to earn a certain amount of interest over the agreed term. If you repay the loan early, the lender misses out on that interest income. The ERC is designed to compensate the lender for this loss.

4. Types of Mortgages with Early Repayment Charges

Not all mortgages come with early repayment charges, but they are common in certain types of products. Understanding which mortgages are more likely to have ERCs can help you make an informed decision when choosing a mortgage.

4.1 Fixed-Rate Mortgages

Fixed-rate mortgages are the most common type of loan that includes ERCs. Because the interest rate is fixed for a set period, lenders impose ERCs to prevent borrowers from leaving the deal early if interest rates drop.

4.2 Tracker Mortgages

Tracker mortgages, which follow the Bank of England’s base rate, can also come with ERCs, especially if they include a period where the rate is discounted.

4.3 Discounted Variable-Rate Mortgages

These mortgages start with a lower rate than the lender’s standard variable rate, but they often include ERCs during the discount period.

4.4 Flexible and Offset Mortgages

Some flexible and offset mortgages allow overpayments without penalty, but they may have ERCs if you repay the entire loan early.

5. How Are Early Repayment Charges Calculated?

ERCs are usually calculated as a percentage of the outstanding mortgage balance. The percentage often depends on how long you have had the mortgage and how much time is left in the fixed or discounted period.

5.1 Example Calculation

If you have a £200,000 mortgage and your ERC is 3%, the charge would be £6,000 if you repay the mortgage early during the period when the 3% charge applies.

5.2 Tapered Charges

Some lenders offer tapered ERCs, where the percentage charge decreases over time. For instance, a 5-year fixed-rate mortgage might have an ERC of 5% in the first year, 4% in the second year, and so on.

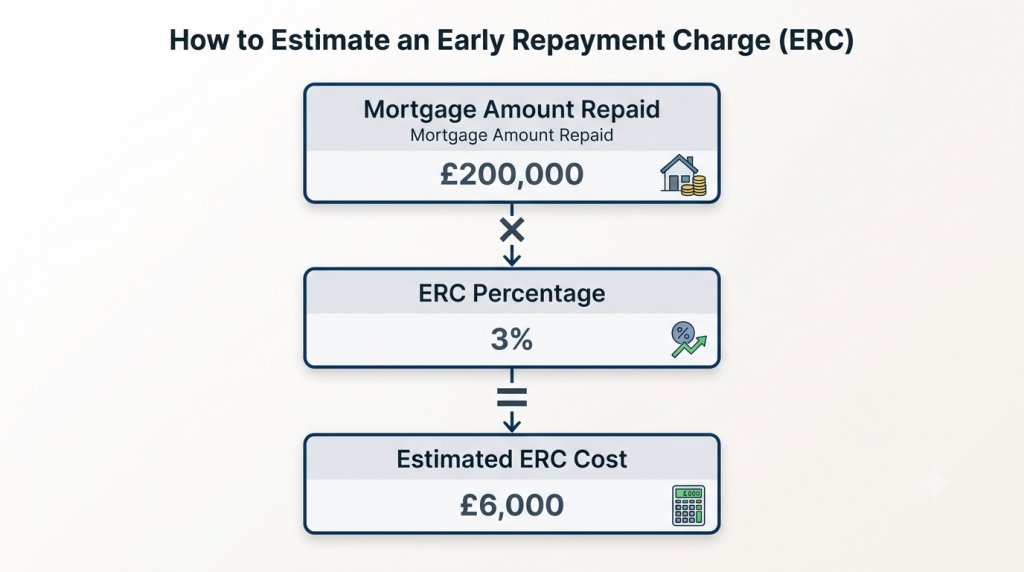

How Is an Early Repayment Charge Calculated?

Early Repayment Charge Calculation Example

Your estimated early repayment charge is calculated by multiplying the amount being repaid by the ERC percentage.

Mortgage balance × ERC percentage = Estimated early repayment charge

Example:

Mortgage balance being repaid: £200,000

ERC percentage: 3%

Calculation:

£200,000 × 3% = £6,000

Estimated early repayment charge: £6,000

early-repayment-charge-calculation-example.webp

How Is an Early Repayment Charge Calculated?

6. Pros and Cons of Early Mortgage Repayment

Paying off your mortgage early has its benefits, but it’s important to weigh these against the potential costs of ERCs.

6.1 Pros of Early Mortgage Repayment

- Interest Savings: Paying off your mortgage early can save you thousands in interest payments over the life of the loan.

- Debt-Free Living: Becoming mortgage-free can provide peace of mind and financial freedom.

- Increased Equity: Paying off your mortgage early increases your home equity, which can be beneficial if you plan to sell or take out a home equity loan.

6.2 Cons of Early Mortgage Repayment

- ERCs: The most significant downside is the potential for hefty early repayment charges.

- Opportunity Cost: The money used to pay off your mortgage early could be invested elsewhere, potentially earning a higher return than the interest saved.

- Liquidity Issues: Paying off your mortgage early could tie up your money in your home, reducing your cash flow for other expenses or investments.

7. How to Avoid Early Repayment Charges

There are several strategies you can use to avoid or minimize ERCs, allowing you to repay your mortgage early without incurring significant penalties.

7.1 Make Use of Overpayment Allowances

Many lenders allow you to overpay a certain percentage of your mortgage each year without incurring ERCs. Taking advantage of this can reduce your balance and the interest you pay over time.

7.2 Time Your Repayment

If your fixed or discounted period is about to end, consider waiting until it’s over before repaying the mortgage. After this period, many mortgages allow for full repayment without penalties.

7.3 Port Your Mortgage

If you’re moving house, some lenders allow you to “port” your existing mortgage to a new property, avoiding ERCs.

7.4 Negotiate with Your Lender

In some cases, lenders may be willing to waive or reduce the ERC, particularly if you are switching to another product with the same lender.

8. What to Do If You’re Hit with an ERC

If you’re facing an ERC, there are steps you can take to manage the situation and potentially reduce the impact.

8.1 Review Your Mortgage Agreement

Check the terms of your mortgage agreement to understand the ERC’s specific details, including how it’s calculated and any conditions that may reduce the charge.

8.2 Contact Your Lender

Speak with your lender to see if there’s any flexibility in the ERC. In some cases, lenders may offer a discount or allow you to avoid the charge under certain circumstances.

8.3 Seek Financial Advice

If you’re unsure how to proceed, consider seeking advice from a financial advisor who can help you weigh the costs and benefits of paying off your mortgage early.

9. ERCs and Remortgaging

Remortgaging, or switching your mortgage to a different deal or lender, is a common way to save money on interest. However, if you’re still in the fixed or discounted period of your current mortgage, you might face ERCs.

9.1 Weighing the Costs

When considering remortgaging, compare the savings you’ll make on the new mortgage against the cost of the ERC. In some cases, the savings from a lower interest rate can outweigh the ERC.

9.2 Timing Your Remortgage

If possible, time your remortgage to coincide with the end of your current mortgage’s fixed or discounted period. This can help you avoid ERCs entirely.

9.3 Porting Your Mortgage

As mentioned earlier, porting your mortgage to a new property can allow you to switch homes without incurring an ERC, provided your lender allows it.

10. Is Paying Off Your Mortgage Early Worth the ERC?

Deciding whether to pay off your mortgage early, despite the ERC, depends on various factors, including your financial goals, the size of the ERC, and the potential interest savings.

10.1 Calculating the Break-Even Point

To determine if paying off your mortgage early is worth the ERC, calculate the break-even point. This is the point at which the interest savings from paying off the mortgage outweigh the cost of the ERC.

10.2 Considering Your Financial Goals

Think about your long-term financial goals. If being debt-free is a priority, paying off your mortgage early might be worth the ERC. However, if you can invest the money elsewhere for a higher return, it might be better to keep the mortgage and avoid the ERC.

10.3 The Impact of Inflation

Inflation reduces the real value of money over time. If inflation is high, the real cost of your mortgage debt decreases, which might make it less urgent to pay off the mortgage early.

11. Case Studies: Examples of ERCs in Practice

To better understand how ERCs can affect homeowners, let’s look at some hypothetical case studies.

11.1 Case Study 1: The Fixed-Rate Mortgage

John has a fixed-rate mortgage with a 5-year term and an ERC of 5% in the first year, decreasing by 1% each subsequent year. After three years, John receives a large inheritance and wants to pay off the mortgage. However, the ERC is 3%, which amounts to £4,500 on his £150,000 outstanding balance. John decides to pay off the mortgage anyway, as the interest savings over the remaining two years will exceed the ERC.

11.2 Case Study 2: The Tracker Mortgage

Sarah has a tracker mortgage with an ERC of 2% for the first two years. With only six months left on the ERC period, Sarah finds a better mortgage deal. She decides to wait until the ERC period ends before switching, saving herself £3,000 in fees.

11.3 Case Study 3: The Remortgage

David wants to remortgage to a lower interest rate, but his current mortgage has an ERC of 4%, which would cost him £8,000. After calculating the potential savings, David realizes that the new deal will save him £10,000 over the next five years, so he decides to go ahead with the remortgage despite the ERC.

12. Frequently Asked Questions about Early Repayment Charges

12.1 What Is an Early Repayment Charge?

An early repayment charge is a fee charged by lenders when you repay your mortgage early or make overpayments that exceed the allowed limit.

12.2 How Can I Avoid Early Repayment Charges?

To avoid early repayment charges, you can make use of overpayment allowances, time your repayment to coincide with the end of the fixed or discounted period, or port your mortgage if you’re moving house.

12.3 Are Early Repayment Charges Always a Percentage of the Loan?

Yes, ERCs are typically a percentage of the outstanding loan balance, but the exact percentage and how it’s applied can vary depending on the lender and the mortgage product.

12.4 Can I Negotiate the Early Repayment Charge with My Lender?

In some cases, lenders may be willing to negotiate the ERC, particularly if you’re switching to another product with the same lender or if you have extenuating circumstances.

12.5 Is It Worth Paying Off My Mortgage Early If There’s an ERC?

Whether it’s worth paying off your mortgage early depends on the size of the ERC, the interest savings you’ll achieve, and your long-term financial goals.

Are Early Repayment Charges Legal in the UK?

Yes, early repayment charges (ERCs) are legal in the UK, provided they are clearly disclosed, properly calculated, and comply with mortgage regulation requirements. Mortgage lenders are allowed to charge an ERC because repaying a mortgage early can result in financial losses for the lender, particularly when a borrower leaves a fixed-rate or discounted mortgage deal before the agreed term ends.

However, lenders cannot apply ERCs without informing borrowers. The charge must be explained before the mortgage agreement is completed, allowing customers to understand the potential costs of repaying their mortgage early.

FCA Rules on Early Repayment Charges

Mortgages regulated by the Financial Conduct Authority (FCA) must follow specific requirements regarding early repayment charges. Lenders must ensure that ERCs are transparent and that borrowers receive sufficient information before committing to a mortgage product.

Under FCA mortgage conduct rules, lenders must make it clear:

- When an early repayment charge applies

- How the charge is calculated

- How long the ERC period lasts

- The maximum amount the borrower may need to pay

The purpose of these rules is to ensure borrowers can make informed decisions when choosing a mortgage and understand the potential costs of changing or repaying their mortgage early.

ERCs Must Be Disclosed Before You Take a Mortgage

Mortgage lenders must provide information about early repayment charges through mortgage documentation, including the Mortgage Illustration (also known as a European Standardised Information Sheet for some products).

This document should outline:

- The circumstances where an ERC may be payable

- The percentage or calculation method used

- An example of the potential charge

- The period during which the charge applies

Before agreeing to a mortgage, borrowers should check the ERC section carefully, particularly if they expect they may sell their property, refinance, or make large overpayments during the initial mortgage term.

Are Early Repayment Charges Reasonable?

While lenders can legally charge ERCs, the amount charged must be reasonable and linked to the financial loss the lender expects to incur as a result of early repayment.

The FCA requires regulated mortgage early repayment charges to be expressed as a cash amount and to represent a reasonable pre-estimate of the lender’s costs. This means ERCs should not simply act as a penalty; they are intended to compensate the lender for costs associated with the borrower leaving the mortgage agreement early.

For example:

- A £200,000 mortgage with a 5% ERC could result in a maximum charge of £10,000.

- The same mortgage with a 2% ERC could result in a maximum charge of £4,000.

The actual amount payable will depend on the lender’s terms, the outstanding mortgage balance, and the point at which the mortgage is repaid.

Can a Lender Charge an ERC When Selling a Property?

Yes, an ERC may still apply if you sell your property before the end of your mortgage deal. Many borrowers assume that selling their home automatically removes the charge, but fixed-rate and discounted mortgage products often include ERCs to protect the lender during the initial deal period.

Before selling or refinancing, it is worth calculating:

- The total ERC payable

- The remaining mortgage term

- Potential interest savings from switching products

- Whether waiting until the ERC period ends would be more cost-effective

For property investors and buy-to-let landlords, understanding ERCs is particularly important because early repayment charges can affect refinancing strategies, portfolio restructuring, and property sale decisions.

Key Takeaway

Early repayment charges are legal in the UK, but mortgage lenders must follow strict rules around transparency, disclosure, and calculation. Before taking out a mortgage, borrowers should understand when an ERC applies, how much it could cost, and whether the potential benefits of repaying early outweigh the charge.

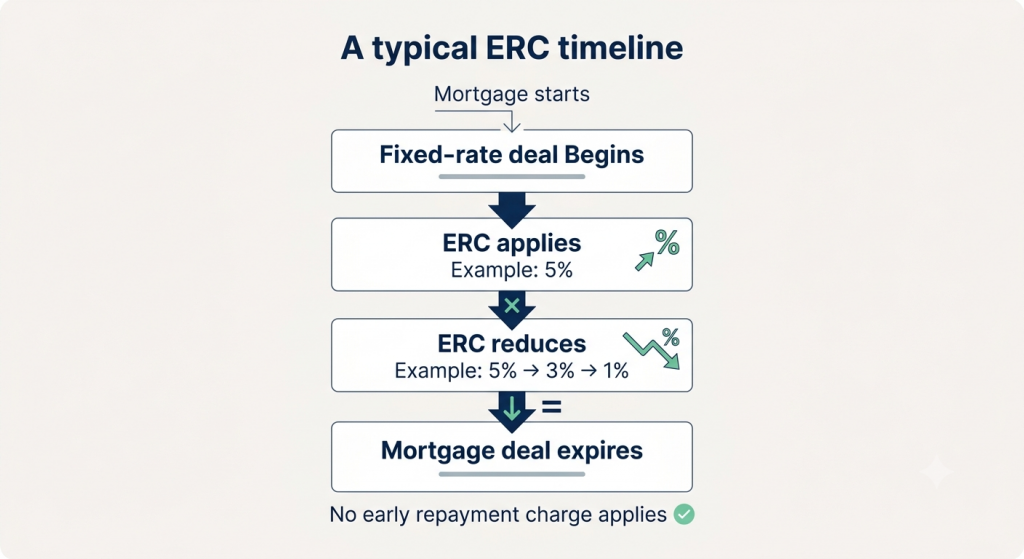

When Do Early Repayment Charges Apply

The length of time an ERC applies depends on your mortgage deal. Most early repayment charges apply during an initial fixed-rate or discounted period and reduce or disappear once the deal ends.

Early Repayment Charges on Buy-to-Let Mortgages

Early repayment charges (ERCs) are particularly important for buy-to-let investors because property investment strategies often involve refinancing, selling, or restructuring finance before the end of a mortgage deal. Unlike many residential homeowners, landlords frequently make strategic decisions that depend on timing, such as refinancing after completing improvements, releasing equity, or moving properties within a portfolio.

Understanding how ERCs work on buy-to-let mortgages can help landlords avoid unexpected costs and make better-informed investment decisions.

Fixed-Rate Buy-to-Let Mortgages and Early Repayment Charges

Many buy-to-let mortgages are arranged on fixed-rate deals, where the interest rate is secured for a set period, commonly two, three, or five years. During this fixed period, lenders often apply an early repayment charge if the mortgage is repaid early.

For landlords, an ERC may become payable if they:

- Sell a rental property before the fixed-rate period ends

- Refinance with another lender

- Switch mortgage products early

- Repay a significant portion of the mortgage balance

The charge is usually calculated as a percentage of the outstanding mortgage balance or the amount being repaid. For example, a £250,000 buy-to-let mortgage with a 3% ERC could result in a potential charge of £7,500.

Before choosing a fixed-rate BTL mortgage, investors should consider how long they realistically expect to hold the property and whether their investment strategy may require flexibility.

Early Repayment Charges for Portfolio Landlords

Portfolio landlords with multiple properties need to pay particular attention to ERCs because mortgage decisions on one property can affect wider investment plans.

A landlord may need to refinance or restructure borrowing in order to:

- Improve cash flow across their portfolio

- Release equity for additional purchases

- Consolidate lending arrangements

- Adjust loan-to-value ratios

- Fund property improvements

Multiple ERCs across several properties can create a significant cost. For example, a landlord refinancing five properties with separate fixed-rate mortgages could face substantial charges if each mortgage remains within its ERC period.

Portfolio investors should therefore consider mortgage expiry dates as part of their long-term property strategy and maintain a clear schedule of when refinancing opportunities become available.

Early Repayment Charges During a BRR Strategy

The Buy, Refurbish, Refinance (BRR) strategy is one of the most common approaches used by property investors, but ERCs can have a major impact on the timing and profitability of the strategy.

During a BRR project, investors typically:

- Purchase an undervalued property

- Complete refurbishment works

- Increase the property’s value

- Refinance based on the improved valuation

- Release capital for the next investment

However, refinancing too soon after purchase may trigger an early repayment charge on the original mortgage.

Investors should calculate whether the benefit of refinancing outweighs the ERC cost. Factors to consider include:

- Additional borrowing available after refurbishment

- Improved rental income

- Future investment opportunities created by released capital

- The cost of paying the ERC immediately

In some cases, paying an ERC may be worthwhile if refinancing allows an investor to recycle capital into another profitable project. In other situations, waiting until the ERC period expires may produce a better overall return.

Selling a Buy-to-Let Property Before Mortgage Expiry

Landlords may decide to sell a rental property before the end of a mortgage deal for many reasons, including:

- Changing investment strategy

- Reducing exposure to a particular area

- Taking profits from capital growth

- Responding to changes in taxation or regulation

- Rebalancing a property portfolio

However, selling before the mortgage term ends does not usually remove the lender’s right to charge an ERC.

Before selling, landlords should calculate:

- The expected ERC cost

- Estate agent and legal fees

- Outstanding mortgage balance

- Potential capital gains tax implications

- Whether delaying the sale until the ERC expires would improve returns

A property sale that appears profitable may become less attractive once early repayment charges are included.

Capital Raising and Early Repayment Charges

Many property investors use refinancing to release equity from existing properties and fund further purchases, refurbishments, or business expansion.

Capital raising can be an effective investment strategy, but landlords need to consider whether their current mortgage allows additional borrowing without triggering ERCs.

Before refinancing for capital raising, investors should review:

- Current mortgage balance

- Available equity

- Existing ERC period

- New mortgage costs

- Potential increase in monthly repayments

A common mistake is focusing only on the amount of capital released while overlooking the cost of leaving the existing mortgage early.

Timing Refinancing After Refurbishment

Timing is critical for investors who complete refurbishment projects.

After improving a property, landlords may want to refinance quickly to access the increased value. However, if the existing mortgage is still within its ERC period, the cost of refinancing early could reduce the overall return.

A useful approach is to compare:

Option 1: Refinance immediately

Potential benefits:

- Access released equity sooner

- Start the next investment project earlier

- Improve borrowing capacity

Potential drawbacks:

- Pay an ERC

- Pay new mortgage arrangement costs

- Possible valuation and legal fees

Option 2: Wait until the ERC period ends

Potential benefits:

- Avoid early repayment penalties

- Reduce refinancing costs

Potential drawbacks:

- Capital remains tied up

- Slower portfolio growth

The best option depends on the numbers. Investors should calculate the additional return generated by accessing capital sooner and compare it against the cost of paying the ERC.

Key Considerations for Buy-to-Let Investors

Early repayment charges should be treated as part of the overall investment calculation rather than simply an unexpected expense.

Before taking out a buy-to-let mortgage, investors should consider:

- How long they expect to hold the property

- Whether they plan to refurbish and refinance

- Future portfolio expansion plans

- Potential need for capital raising

- Mortgage flexibility alongside headline interest rates

For property investors, the cheapest mortgage rate is not always the most suitable option. A mortgage with lower ERCs or greater flexibility may provide better long-term value by allowing faster adaptation as investment plans change.

| Mortgage type | ERC likely? |

|---|---|

| Fixed-rate mortgage | Yes |

| Tracker mortgage | Sometimes |

| Variable mortgage | Sometimes |

| Lifetime tracker | Usually no |

| Standard variable rate | Usually no |

| Mortgage balance | ERC | Cost |

|---|---|---|

| £150,000 | 5% | £7,500 |

| £200,000 | 3% | £6,000 |

| £300,000 | 2% | £6,000 |

Frequently Asked Questions

→ Can I avoid an early repayment charge?

→ Are ERCs negotiable?

→ Do ERCs apply when selling a house?

→ Can I add an ERC to a new mortgage?

→ Do buy-to-let mortgages have ERCs?

→ When does an ERC expire?

→ Is it worth paying an ERC to remortgage?

Frequently Asked Questions About Early Repayment Charges

Early repayment charges (ERCs) are one of the most important factors to consider before repaying a mortgage, switching lenders, selling a property, or refinancing. Below are answers to the most common questions borrowers and property investors ask about ERCs.

Can I avoid an early repayment charge?

In some situations, it may be possible to avoid paying an early repayment charge. The simplest way is to wait until your mortgage deal reaches the end of its ERC period before repaying or switching products.

Other ways borrowers may reduce or avoid ERC costs include:

- Choosing a mortgage product with no early repayment charge

- Using any annual overpayment allowance provided by the lender

- Porting your mortgage to a new property (if permitted by your lender)

- Waiting until the fixed-rate or discounted period expires

- Negotiating mortgage terms that provide greater flexibility

Before making any changes, check your mortgage offer or speak with your lender because ERC rules vary between mortgage products.

Are early repayment charges negotiable?

Generally, early repayment charges are not negotiable once they are included in your mortgage agreement. Lenders calculate ERCs according to the terms of the mortgage product and regulatory requirements.

However, borrowers may have flexibility before taking out a mortgage by comparing products with:

- Lower ERC percentages

- Shorter fixed-rate periods

- More generous overpayment allowances

- No early repayment charges

For property investors, choosing a mortgage with greater flexibility can sometimes be more valuable than choosing the lowest initial interest rate.

Do early repayment charges apply when selling a house?

Yes, an early repayment charge may apply if you sell your property before your mortgage deal ends.

Many borrowers assume that selling automatically removes the charge, but if you repay a fixed-rate or discounted mortgage early, the lender may still apply an ERC.

Before selling, consider:

- The remaining ERC period

- The outstanding mortgage balance

- The estimated ERC cost

- Whether delaying the sale could reduce costs

Some mortgages are portable, meaning you may be able to transfer the mortgage to another property and avoid the ERC, subject to lender approval.

Can I add an ERC to a new mortgage?

No, an early repayment charge from an existing mortgage cannot usually be added to a new mortgage automatically.

However, some lenders may allow borrowers to include certain mortgage-related costs within a new mortgage arrangement. This depends on affordability assessments, lender criteria, and the terms of the new mortgage.

Borrowers should compare the cost of:

- Paying the ERC upfront

- Adding costs to a new mortgage

- Waiting until the ERC period ends

Adding costs to a mortgage may increase the total interest paid over time.

Do buy-to-let mortgages have early repayment charges?

Yes, many buy-to-let mortgages include early repayment charges, particularly fixed-rate and discounted mortgage products.

ERCs are especially important for landlords because property investment strategies often involve refinancing, capital raising, refurbishment projects, and portfolio restructuring.

Buy-to-let investors should consider ERCs when planning:

- Buy, Refurbish, Refinance (BRR) projects

- Portfolio expansion

- Equity release

- Property sales

- Mortgage refinancing

A mortgage with greater flexibility may be more suitable for investors who expect to make changes to their portfolio.

When does an early repayment charge expire?

An early repayment charge normally expires when the initial mortgage deal ends. For example, if you have a five-year fixed-rate mortgage, the ERC usually applies during that five-year period and ends when the fixed-rate term finishes.

However, the exact date depends on your mortgage agreement.

Before switching mortgages or repaying early, check:

- The date your ERC period ends

- The remaining ERC percentage

- Any lender-specific conditions

Some lenders reduce the ERC percentage each year, while others apply a fixed charge throughout the mortgage deal.

Is it worth paying an ERC to remortgage?

Whether paying an ERC is worthwhile depends on the potential savings or benefits gained from switching mortgage products.

Paying an ERC may make financial sense if:

- A new mortgage offers significantly lower interest rates

- You can release equity for further investment

- Refinancing improves your cash flow

- The long-term savings exceed the ERC cost

However, you should compare the total cost of switching, including:

- Early repayment charge

- New mortgage arrangement fees

- Legal costs

- Valuation fees

- Any changes to monthly repayments

For property investors, the decision should be based on the overall return on investment rather than the ERC cost alone.

Key Takeaway

Early repayment charges can represent a significant cost, but understanding when they apply and how they are calculated allows borrowers and investors to make better mortgage decisions. Always review your mortgage terms before repaying early, refinancing, or selling a property.

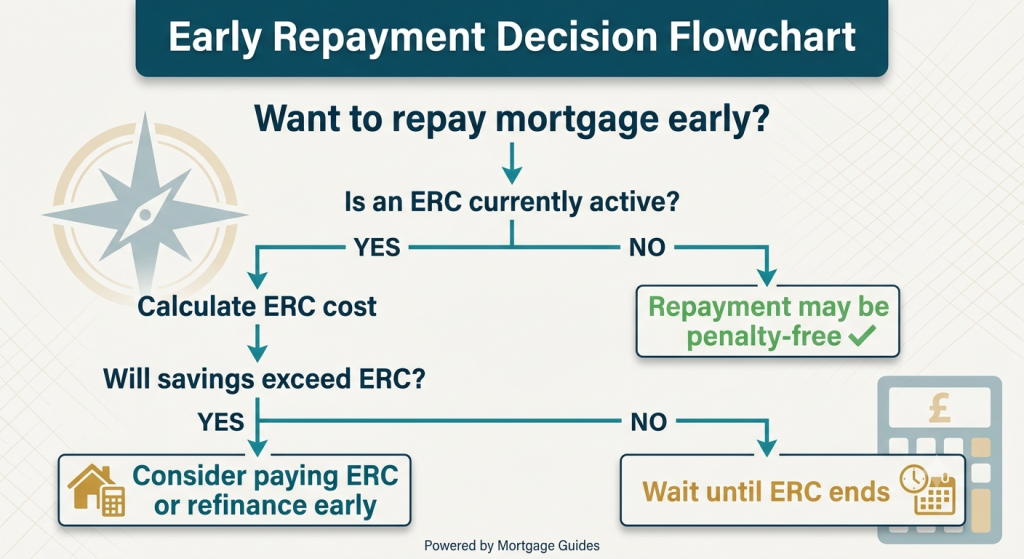

Should You Pay an Early Repayment Charge?

Before repaying your mortgage early, refinancing, or selling a property, consider whether the financial benefit outweighs the cost of the ERC.

Use the decision guide below:

13. External Resources for Further Reading

For more information on early repayment charges and how they might affect your mortgage, consider the following resources:

- MoneySavingExpert for tips on overpaying your mortgage and managing early repayment charges.

- Which? for detailed advice on choosing the right mortgage and understanding the costs involved.

- Citizens Advice for guidance on mortgages, including dealing with early repayment charges and other fees.

14. Conclusion

Early repayment charges on mortgages can be a significant consideration for homeowners looking to pay off their mortgage early or switch to a better deal. While these charges can be substantial, understanding how they work and planning your repayment strategy can help you minimize their impact. Whether you’re considering overpaying, remortgaging, or simply want to be prepared for the future, being informed about ERCs will allow you to make the best financial decisions for your situation.

Remember to weigh the pros and cons carefully, consider your long-term financial goals, and seek advice if needed to ensure that any decision you make aligns with your overall financial strategy.

Leave a Reply